Holiday Insurance Guide · 2026

Holiday Insurance

Post Office UK:

The Complete 2026 Guide

Everything you need to know before you buy — cover levels, real prices, pre-existing conditions, claims, and the honest truth about what’s not covered.

Here is the single most important thing to know about holiday insurance: it is not a box-ticking exercise. It is the difference between coming home from a medical emergency with a suntan and coming home with a debt that takes years to clear. A hospital admission in the USA, for example, can exceed £100,000. A missed flight, a stolen suitcase, or a broken ankle on a ski slope can each cost thousands. The question is never whether you need cover — it is whether the cover you buy is actually good enough.

The Post Office has been selling travel insurance to UK holidaymakers for decades, and today it is one of the most searched-for providers in the country. But popular does not automatically mean right for you. This guide strips away the marketing language and tells you exactly what you are getting — and crucially, what you are not.

This article contains information about financial products. While every effort has been made to ensure accuracy as of May 2026, always read the official policy wording at postoffice.co.uk before purchasing. Insurance terms can change without notice.

📋 In This Guide

- What is Post Office Holiday Insurance?

- The Three Cover Levels Explained

- What’s Actually Covered?

- Real 2026 Prices

- Pre-Existing Medical Conditions

- Single Trip vs Annual vs Backpacker

- Optional Add-Ons Worth Buying

- How to Make a Claim

- GHIC vs Travel Insurance

- Who Should Buy It — and Who Shouldn’t

- Frequently Asked Questions

1. What is Post Office Holiday Insurance?

Post Office travel insurance — also called holiday insurance — is a financial protection product sold by the Post Office, one of the UK’s most trusted brands. The underlying insurance is provided by specialist underwriters, but the product is distributed and supported by Post Office Ltd, which means you can buy it online, by phone, or in person at a Post Office branch.

Paid out in claims over five years

Defaqto rating for Premier cover

Your Money Awards winner (incl. 2026)

The Post Office has won the “Best Travel Insurance Provider” award at the Your Money Awards in 2021, 2022, 2023, 2025, and 2026 — a track record that matters, because it reflects sustained satisfaction rather than a one-off win. Its Premier cover level holds a Defaqto 5-star rating and a Moneyfacts Five Star rating for 2024 and 2025.

But awards tell you about reputation, not suitability. Let’s look at what you actually get.

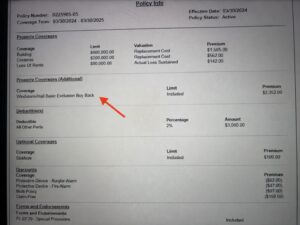

2. The Three Cover Levels Explained

Post Office offers three tiers of holiday insurance: Economy, Standard, and Premier. Each tier unlocks progressively higher limits and broader protections. Here’s how the key figures compare:

Entry Level

Mid-Range

Recommended

Economy cover offers only £1,000 cancellation — barely enough to cover a flight, let alone a full package holiday. The £150 single-item limit means your laptop, camera, or smartphone won’t be adequately covered. Economy is fine for a budget day trip; it’s inadequate for a two-week family holiday abroad.

3. What’s Actually Covered?

Understanding the breadth of coverage is as important as knowing the limits. Here’s a plain-English breakdown of the main protections across Post Office holiday insurance policies:

-

🏥

Emergency Medical Expenses & Repatriation

Up to £15 million on Premier cover. This is the most critical element — overseas medical treatment and the cost of flying you home (repatriation) are covered. The 24/7 emergency assistance line is available on all policies. -

✈️

Cancellation & Curtailment

If you have to cancel before departure or cut your trip short due to illness, redundancy, bereavement, or other specified reasons, you can claim back non-refundable costs — up to £5,000 on Premier policies. Cancellation cover begins the moment you purchase the policy. -

🧳

Baggage & Personal Belongings

Covers loss, theft, or damage to your luggage and contents. Note single-item limits (£150–£400 depending on tier) — if you travel with high-value electronics, add gadget cover separately. -

⏰

Travel Delay

If your international departure is delayed by 4 hours or more due to reasons such as bad weather, industrial action, or technical faults, you receive a delay benefit — paid per full 4-hour block, up to 12 hours maximum. -

🚪

Missed Departure (Standard & Premier only)

If an accident, breakdown, or public transport failure causes you to miss your flight or connection, Post Office covers additional travel and accommodation costs to get you to your destination. -

⚖️

Personal Liability

Covers legal costs and compensation if you accidentally injure someone or damage their property while abroad. Available across all cover levels. -

🦠

Covid-19 Cover

Cancellation cover applies if a medical practitioner certifies you too ill to travel due to Covid-19, or if you or a travelling companion are hospitalised. Medical expenses if you contract Covid-19 abroad are also covered. -

👨⚕️

Medical Assistance Plus (Free on All Policies)

Powered by Air Doctor, this gives you access to outpatient medical support while travelling — health professionals available digitally, wherever you are in the world.

4. Real 2026 Prices

Pricing varies based on your age, destination, trip duration, and health history. The figures below reflect independently verified 2026 quotes for healthy adults with no declared medical conditions.

| Policy Type & Destination | Economy | Standard | Premier |

|---|---|---|---|

| Single Trip – 7 days Europe (e.g. Spain) | ~£24 | ~£32 | ~£42 |

| Single Trip – 7 days USA/Canada | ~£38 | ~£52 | ~£68 |

| Annual Multi-Trip – Europe | ~£55 | ~£79 | ~£105 |

| Annual Multi-Trip – Worldwide | ~£85 | ~£115 | ~£150 |

| Family (incl. under-18s free) – 7 days Europe | ~£24 | ~£32 | ~£42 |

One of the Post Office’s standout features is that children under 18 are included at no extra cost on family policies. This makes it genuinely competitive for families — the per-head price drops significantly compared to per-person pricing from many other providers.

Prices rise with age and declared medical conditions. If you travel more than twice a year, an annual multi-trip policy almost always represents better value than buying separate single-trip policies.

5. Pre-Existing Medical Conditions: What You Must Know

This is the section that matters most if you or anyone travelling with you has a health condition. Post Office explicitly states that all medical conditions should be declared — even well-managed ones and any prescription medications you take.

Why Declaring Is Non-Negotiable

If you fail to disclose a pre-existing condition and then make a claim — even for something seemingly unrelated — the insurer may void your policy entirely. You could face the full cost of overseas medical care alone. The stakes are too high to cut corners here.

What Happens When You Declare?

Post Office considers all pre-existing conditions through a medical screening process. In many cases, cover can be arranged for declared conditions, though it may cost more. If Post Office cannot offer cover for a serious condition, they are required to direct you to the Money and Pensions Scheme (MaPS) directory — a regulated service that can connect you with specialist insurers who may be able to help. You can also call MaPS on 0800 138 7777.

Even if a condition is well managed — for example, controlled type 2 diabetes or stable angina — it must be declared. “Stable” does not mean “excluded from declaration.” Read the policy wording section on medical conditions carefully or call the Post Office to clarify before purchasing.

Cancellation and Pre-Existing Conditions

If you need to cancel a trip due to a pre-existing condition worsening, the policy wording typically requires a medical practitioner to confirm in writing that, at the time you purchased the policy, there was no substantial likelihood of the condition deteriorating to the degree that cancellation became necessary. This is important: it means buying insurance early — not weeks before departure — is critical for maximum protection.

6. Single Trip vs Annual vs Backpacker: Which Do You Need?

-

🗺️

Single Trip Insurance

Covers one specific journey from departure to return. Ideal for occasional travellers. Trips can be covered for up to 365 days in length. This is the most straightforward option and usually the cheapest entry point. -

🔄

Annual Multi-Trip Insurance

One policy covers all trips within a 12-month period. Economy and Standard policies cap individual trips at 17 days; Premier extends this to 31 days. Best value for anyone taking two or more holidays per year. Also covers UK trips. -

🎒

Backpacker Insurance

A single-trip policy designed for extended travel, covering up to 18 months. Built for gap year travellers, career-breakers, or anyone planning a long-haul adventure through multiple countries. Particularly cost-effective compared to stringing multiple single-trip policies together.

Travelling once this year? → Single Trip. Travelling twice or more? → Annual (it usually pays for itself by the third trip). Going away for months? → Backpacker. Taking the family somewhere once? → Single Trip family policy (children under 18 are free).

7. Optional Add-Ons: The Ones Worth Buying

Post Office lets you customise your policy with optional extras. Some are genuinely valuable; others are less so depending on your trip. Here’s an honest assessment:

| Add-On | Worth It? | Best For |

|---|---|---|

| Winter Sports Cover | ✓ Essential | Skiing, snowboarding, any slope activity. Mandatory — standard policies exclude winter sports entirely. |

| Gadget Cover | ✓ Recommended | Anyone travelling with a smartphone, laptop, or camera worth more than the £150–£400 single-item limit. |

| Cruise Cover | ✓ If cruising | Covers missed port departures, cabin confinement, and other cruise-specific risks not in standard policies. |

| Excess Waiver | ◐ Consider it | Removes the £125 per-claim excess. Worth it for families or anyone likely to make smaller claims. |

| Airspace Disruption / Natural Catastrophe | ◐ Optional | Covers cancellations due to volcanic ash, terrorist acts, or Covid-19. Peace of mind for long-haul travel. |

| Trip Extension (45 or 60 days) | ✓ If needed | Standard single-trip policies cover up to 31 days. If your trip is longer, you must extend — or you’ll have no cover. |

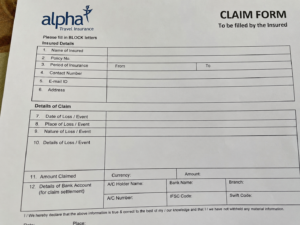

8. How to Make a Claim

Knowing how to claim before you need to is smart preparation. The claims process at Post Office is straightforward — but following the right steps in the right order is essential to avoiding delays or rejections.

Contact the Emergency Assistance Line First (Medical Emergencies)

For any medical emergency abroad, call the 24/7 emergency assistance line before seeking treatment where possible. Failing to notify them could affect your claim. They can authorise treatment, arrange hospital direct billing, and organise repatriation if needed.

Gather Your Evidence

Keep all receipts, medical reports, police reports (for theft), and booking confirmations. Without evidence of the loss or expense — and evidence of ownership for belongings — claims can be reduced or refused. For theft, a police report within 24 hours is typically required.

Claim via Your Travel Provider First (Where Applicable)

Post Office policy requires you to contact your airline, tour operator, or card provider for refunds before claiming from insurance. This applies to cancelled flights and accommodation — insurance is a last resort, not a first port of call.

Submit Your Claim Online or by Phone

Claims can be submitted through the Post Office website or by calling their claims line. Have your policy number, trip details, and all supporting documentation ready. Online claims are typically processed faster.

Track and Follow Up

Keep a log of every communication — dates, names, reference numbers. If a claim is rejected unfairly, you have the right to escalate to the Financial Ombudsman Service (FOS), which is free to use.

9. GHIC vs Travel Insurance: Why You Still Need Both

Many people believe their UK Global Health Insurance Card (GHIC) — which replaced the EHIC after Brexit — makes travel insurance unnecessary for European travel. This is one of the most dangerous misconceptions in holiday planning.

| Protection | GHIC/EHIC | Travel Insurance |

|---|---|---|

| Emergency medical treatment (state facilities) | ✓ Yes | ✓ Yes |

| Repatriation (flying you home) | ✗ No | ✓ Yes |

| Private medical care abroad | ✗ No | ✓ Yes |

| Trip cancellation | ✗ No | ✓ Yes |

| Lost or stolen luggage | ✗ No | ✓ Yes |

| Flight delays & missed departures | ✗ No | ✓ Yes (Standard+) |

| Cover in Iceland, Norway, Switzerland | ✗ No (post-Brexit) | ✓ Yes |

The GHIC gives you access to state-provided healthcare in EU countries at the same cost as a local resident. It does not cover the often enormous cost of getting you home, nor does it cover anything outside the medical emergency itself. Repatriation alone — a specialist air ambulance flight back to the UK — can cost £50,000 or more.

Carry your GHIC card as a backup — but always travel with a proper insurance policy as your primary protection. The GHIC reduces costs for the insurer in Europe (which can sometimes lower your premiums), but it is not a substitute.

10. Who Should Buy Post Office Holiday Insurance?

Our Honest Verdict

Post Office holiday insurance is a strong, well-rounded choice for most UK holidaymakers — particularly at the Premier level, which offers up to £15 million medical cover, £5,000 cancellation, free children’s cover, and a Defaqto 5-star rating at a competitive price point.

It is especially well-suited for families (free under-18 cover is a genuine standout), frequent travellers (the annual policy represents strong value), and older travellers with pre-existing conditions who want a trusted, accessible brand willing to consider all medical conditions.

It is less suitable for travellers with very high-value electronics (single-item limits are modest without the gadget add-on), those planning very long single trips over 31 days without extension, or budget-first travellers who only want Economy cover for a major holiday — the limits there are genuinely thin.

Post Office is a Strong Fit If You Are:

- 👨👩👧👦

A Family TravellerChildren under 18 travel free — a meaningful saving compared to per-person pricing.

- 🌍

A Frequent FlyerAnnual multi-trip policies offer consistent, hassle-free coverage for the full year.

- 🏥

Someone With a Medical ConditionPost Office explicitly considers all conditions and has a clear pathway for declined cases via MaPS.

- 🤝

Someone Who Values TrustThe Post Office brand, award history, and in-branch accessibility give peace of mind that newer fintech insurers may not match.

Consider Alternatives If You:

- 💻

Travel With High-Value TechSingle-item limits (up to £400 on Premier) are modest. Either add gadget cover or look at specialist policies with higher per-item limits.

- 📅

Need Trips Longer Than 31 Days on Annual CoverAnnual Multi-Trip Premier caps trips at 31 days. For longer individual trips, consider single-trip or backpacker policies instead.

- 💷

Are on a Very Tight Budget and Only Need BasicsEconomy cover’s £1,000 cancellation limit is dangerously low for package holidays. If budget is paramount, compare carefully on aggregators like GoCompare or MoneySuperMarket.

11. Frequently Asked Questions