Does homeowners insurance cover hurricane

Home Insurance · NittyBrain

Will Your Homeowners Insurance Actually Show Up When the Hurricane Does?

A honest, no-jargon answer to the question every coastal homeowner asks the night before a storm: does homeowners insurance cover hurricane damage, or are you about to find out the hard way that it doesn’t?

•

Updated July 13, 2026

•

10 min read

There’s a specific kind of dread that sets in when a storm gets a name. You start thinking less about the wind and more about the paperwork — the policy you signed three years ago and never read past the first page. So let’s answer the question plainly, before you need the answer in a hurry: does homeowners insurance cover hurricane damage? Yes, mostly — but “mostly” is doing a lot of work in that sentence, and the gap between what you assume is covered and what’s actually written into your policy is exactly where families get financially blindsided after a storm passes.

We pulled current data from the Insurance Information Institute, the National Association of Insurance Commissioners, and 2026 industry rate filings to give you the real picture — not the marketing-page version. Here’s what actually happens to your claim when a hurricane hits your home.

The short answer

Homeowners insurance covers wind damage from a hurricane — a torn-off roof, shattered windows, siding ripped away, wind-driven rain that pours in through a hole the wind created. It does not cover flooding or storm surge, even when the flood was caused by the same hurricane. And in 19 states, wind claims from a hurricane trigger a separate, more expensive hurricane deductible instead of your normal one.

What Homeowners Insurance Covers When a Hurricane Hits

A standard HO-3 homeowners policy is built around named perils and “all-risk” dwelling coverage, and wind is almost always one of the perils included. That means the following hurricane-related damage is typically covered:

- Roof damage from wind — torn shingles, structural failure, a roof ripped off entirely

- Broken windows and doors caused by wind or wind-driven debris

- Damage to siding, gutters, fences, and detached structures like sheds or garages

- Water damage inside the home, but only if wind first created the opening it entered through

- Fallen trees that damage your home (though not simply removing a tree that missed the house)

- Temporary living expenses if the home becomes uninhabitable during repairs

Notice the pattern: everything on that list traces back to wind. That single distinction — wind versus water — is the whole ballgame in a hurricane claim, and it’s the part most homeowners misunderstand until the adjuster shows up.

The Part No One Warns You About: Flood Is Never Included

Here is the sentence that causes the most heartbreak in post-hurricane claims: standard homeowners insurance does not cover flood damage, storm surge, or water that rises up from outside the home — no matter how directly it was caused by the hurricane. This isn’t a fine-print exclusion buried in one insurer’s policy. It’s a near-universal exclusion across every major carrier, because flood risk is underwritten completely separately from wind risk.

In practice, most catastrophic hurricane losses — the kind that make national news — come from storm surge and inland flooding, not wind alone. That means the homeowners who assumed “I have hurricane coverage” because their policy mentions windstorms are often the same homeowners left without a claim after the water recedes. If you want protection against that specific risk, you need a separate flood policy, either through the National Flood Insurance Program (NFIP) or a private flood insurer, and it typically has a 30-day waiting period before it takes effect — so it has to be in place well before a storm forms, not after one is named.

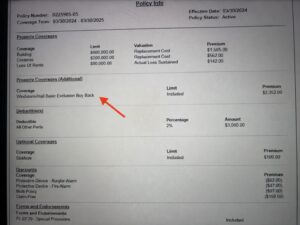

Hurricane Deductibles: The Cost You Won’t See Until You File a Claim

Even when your wind damage is fully covered, you may not pay the same deductible you’d pay for, say, a burst pipe. In 19 states and Washington, D.C., insurers are permitted to apply a separate hurricane or named-storm deductible once a storm meets a specific trigger, such as an official National Weather Service hurricane designation or a specific wind-speed category.

According to the National Association of Insurance Commissioners, the states where this applies are: Alabama, Connecticut, Delaware, Florida, Georgia, Hawaii, Louisiana, Maine, Maryland, Massachusetts, Mississippi, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Texas, and Virginia.

Unlike a standard $500–$2,000 flat deductible, a hurricane deductible is usually a percentage of your home’s insured value — typically 1% to 10%, though some high-risk coastal policies go higher. That percentage-based structure is where homeowners get caught off guard, because the dollar amount scales with your home’s value, not with the size of the damage.

What that looks like in real numbers

Say your home is insured for $300,000 and your policy carries a 5% hurricane deductible. Before your insurer pays a dollar toward wind damage from a hurricane, you’re responsible for the first $15,000 out of pocket. Compare that to a standard $1,000 flat deductible for the exact same repair, and you can see why so many coastal homeowners are underinsured without realizing it.

Florida is the clearest example of how specific this gets: insurers there must offer hurricane deductible options of $500, 2%, 5%, and 10%, and the deductible applies only once per hurricane season, no matter how many named storms hit your home that year. New York, by contrast, only applies its hurricane deductible in certain coastal counties, and the trigger category can differ by insurer. The rules are genuinely not the same from state to state, which is exactly why reading your declarations page matters more than trusting a general assumption.

What Full Hurricane Protection Actually Costs

“Hurricane insurance” isn’t a single product you buy — it’s the combination of your homeowners policy (for wind) and a flood policy (for water), and the two are priced completely independently. Nationally, the average homeowners insurance premium runs about $2,490 a year, and the average NFIP flood policy adds roughly $976 a year, putting full hurricane-risk protection around $3,466 a year for an average home. In high-risk coastal ZIP codes, especially in Florida, that combined number climbs sharply higher, and wind coverage alone can run well into four figures before flood is even added.

That gap between “average” and “coastal” is worth sitting with for a second. If you live near the coast and you’ve been pricing your risk off a national average number, you’re very likely underestimating what full protection costs — and underestimating it right up until the moment you need it most.

Before the Next Storm Forms: A Five-Minute Policy Check

You don’t need to become an insurance expert to protect yourself — you need to answer five specific questions about the policy you already have. Pull out your declarations page and check:

- Does my policy list a separate hurricane, windstorm, or named-storm deductible? If you live in one of the 19 states above, assume yes until you confirm otherwise.

- What percentage is it, and what’s it a percentage of? Usually your Coverage A (dwelling) limit, not your home’s market value — the two can differ significantly.

- Do I have flood insurance at all? Being outside an official flood zone does not mean you’re at low risk — a large share of flood claims come from homes outside mapped high-risk zones.

- What triggers my hurricane deductible? A named storm, a specific category, or an official NWS declaration — the wording changes what you’re actually protected against.

- Is my dwelling coverage limit high enough to rebuild at today’s construction costs? Underinsuring the dwelling value quietly shrinks your flood and wind coverage too, since both often key off that number.

If you can’t answer these confidently, call your agent this week — not during a hurricane watch, when new coverage and policy changes are typically frozen by insurers until the storm passes.

Frequently Asked Questions

Does homeowners insurance cover hurricane damage?

Yes, for wind damage — roof, siding, windows, and wind-driven rain that enters through damage the wind caused. It does not cover flooding or storm surge, which needs a separate flood policy.

Does homeowners insurance cover hurricane flooding?

No. Flood and storm surge are excluded from virtually every standard homeowners policy, regardless of what caused the flooding. You need NFIP or private flood coverage for that risk.

What is a hurricane deductible?

A separate, usually percentage-based deductible (1%–10% of your home’s insured value) that replaces your standard deductible specifically for hurricane wind claims, in the 19 states and D.C. where insurers are permitted to use them.

How much does hurricane insurance cost?

There’s no single policy called “hurricane insurance.” Combining an average homeowners premium (~$2,490/year) with an average NFIP flood policy (~$976/year) puts full protection around $3,466/year nationally — higher in coastal, high-risk areas.

The Bottom Line

Does homeowners insurance cover hurricane damage? For wind, generally yes. For flood, essentially never. And for many coastal homeowners, the deductible that applies to that wind claim is far larger than the one they’ve been picturing in their head. The homeowners who come out of hurricane season financially whole aren’t the ones with the fanciest policy — they’re the ones who actually read the declarations page before the storm had a name.

Take the five-minute check above, call your agent this week, and close the gap between what you assume your policy does and what it’s actually written to do.

Researched and written by NittyBrain

NittyBrain covers insurance and personal finance in plain English, backed by primary sources like the NAIC, the Insurance Information Institute, and current 2026 industry rate data — so you can make decisions based on what your policy actually says, not what you assume it says.

This article is for general informational purposes and isn’t a substitute for reviewing your own policy documents or speaking with a licensed insurance agent about your specific coverage.