Employers’ Liability Insurance UK Cost in 2026: Real Prices, Hidden Factors & How Businesses Can Save Thousands

Running a business in the UK comes with responsibility. The moment you hire an employee — even part-time staff, temporary workers, apprentices, or family members helping in the business — you may legally need employers’ liability insurance. Yet many business owners still struggle with one major question:

How much does employers’ liability insurance UK cost?

How much does employers’ liability insurance UK cost?

The answer is not always straightforward. Some businesses pay less than £100 yearly, while others spend thousands. The difference often depends on industry risk, payroll size, claims history, and the type of work employees perform daily.

This guide explains the real cost of employers’ liability insurance in the UK, what affects pricing, how insurers calculate premiums, practical ways to reduce costs, and a true-to-life scenario showing how one claim nearly destroyed a small business financially.

What Is Employers’ Liability Insurance?

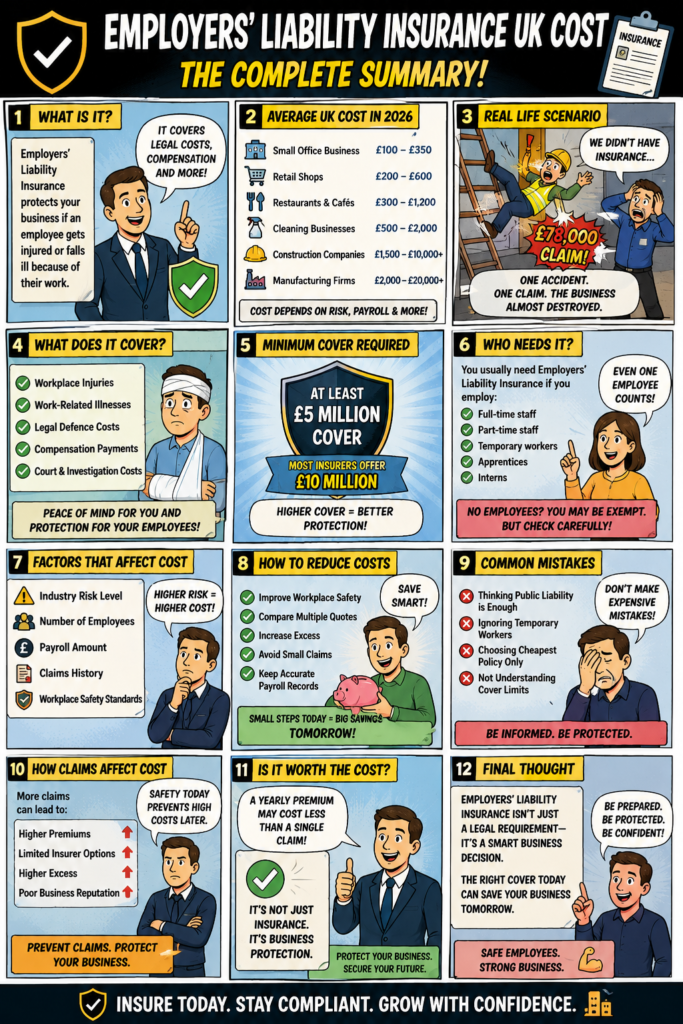

Employers’ liability insurance protects businesses if an employee becomes injured or ill because of their work.

In the UK, this cover is legally required for most businesses under the Employers’ Liability (Compulsory Insurance) Act 1969. If you employ staff and fail to carry valid cover, you could face fines of up to £2,500 per day.

The policy helps pay for:

i. Employee compensation claims

ii. Legal defence costs

iii. Medical expenses

iv. Court settlements

v. Related legal investigations

Without coverage, a single employee injury claim could bankrupt a small company.

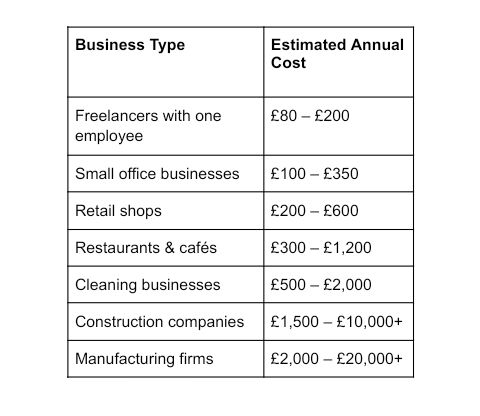

Average Employers’ Liability Insurance UK Cost in 2026

The average employers’ liability insurance UK no cost depends heavily on business type.

Here’s a realistic estimate of what many UK businesses currently pay yearly:

High-risk industries naturally pay more because employee injury claims are more common and often more severe.

Why Employers’ Liability Insurance Costs Vary So Much

Many business analyst owners assume insurers simply choose random prices. In reality, insurers evaluate risk very carefully.

Here are the biggest factors affecting employers’ liability insurance UK cost.

1. Industry Risk Level

This is the largest pricing factor.

An office worker sitting behind a computer all day presents less risk than a roofer working on scaffolding.

Low-Risk Industries

Lower premiums usually apply to:

i. Marketing agencies

ii. Accountants

iii. Consultants

iv. IT companies

v. Online businesses

High-Risk Industries

Higher premiums often apply to:

i. Construction

ii. Warehousing

iii. Manufacturing

iv. Roofing

v. Demolition

vi. Industrial cleaning

The more dangerous the work environment, the more expensive the insurance.

2. Number of Employees

The more employees you have, the greater the chance someone may eventually file a claim.

A business with:

2 employees may pay under £200 yearly while 50 employees may pay several thousand pounds annually.

Insurers calculate exposure partly based on workforce size.

3. Payroll Amount

Payroll matters because it reflects how much labour exposure your business has.

A company paying: £30,000 yearly payroll will usually pay far less than a company with £2 million payroll. Higher payroll often equals more staff hours and greater claim risk.

4. Claims History

Businesses with previous employee injury claims are seen as higher risk. If your company has:

i. Multiple workplace injury claims

ii. Frequent employee accidents

iii. Poor safety records

your premiums may rise significantly. Some insurers may even refuse coverage entirely after repeated claims.

5. Workplace Safety Standards

Businesses with strong safety systems often receive lower premiums. Insurers may reward:

i. Proper staff training

ii. Health & safety procedures

iii. Risk assessments

iv. Protective equipment usage

v. Clean accident records

A safer workplace can dramatically reduce insurance costs over time.

Real-Life Scenario: The Small Electrical Company That Faced a £78,000 Employee Claim

In Manchester, a small electrical contracting business operated with four employees. The owner believed employers’ liability insurance was “too expensive” for such a small team.

To save money, he delayed renewing the policy for several months. During a commercial installation project, one electrician fell from a faulty ladder while wiring ceiling fixtures. He suffered. A fractured spine, long-term nerve damage, partial loss of mobility. The injured employee filed a compensation claim alleging:

i. Unsafe equipment

ii. Poor safety inspection

iii. Negligence by the employer.

Because the business had no active employers’ liability insurance at the time, the owner faced the claim personally. Legal costs and compensation eventually exceeded £78,000.

The company could not survive financially. Within a year. Contracts were lost, cash flow collapsed. The business shut down permanently.

The owner later admitted that renewing the policy would have cost under £1,000 annually.

One missed renewal destroyed the entire company.

What Does Employers’ Liability Insurance Usually Cover?

A standard UK employers’ liability policy commonly covers:

Workplace Injuries if an employee gets injured during work duties.

Example:

i. Falling from ladders

ii. Machinery accidents

iii. Slips and falls

Work-Related Illnesses

Coverage may include illnesses caused by workplace exposure such as:

i. Respiratory conditions

ii. Chemical exposure

iii. Hearing loss

iv. Repetitive strain injuries

Legal Defence Costs.

Even if a claim is false, defending it in court can cost thousands. Insurance often covers:

i. Solicitor fees

ii. Court expenses

iii. Investigation costs

iv. Compensation Payments

If the employer is found legally responsible, the policy may pay compensation awarded to the employee.

What Is the Minimum Cover Required in the UK?

Most UK employers legally need at least – £5 million employers’ liability cover.

However, many insurers automatically provide:£10 million cover. This higher limit offers stronger protection against major claims. Businesses That May Be Exempt.

Some businesses may not require employers’ liability insurance, including:

i. Sole traders with no employees

ii. Certain family-run businesses

iii. Some public organisations.

However, exemptions can be complicated. Even part-time staff, interns, apprentices, or temporary workers may legally count as employees.

Many business owners mistakenly believe they are exempt when they are not.

How Small Businesses Can Reduce Employers’ Liability Insurance Costs

Insurance is necessary, but overpaying is not. Here are proven ways UK businesses lower premiums.

Improve Workplace Safety

Safer businesses usually receive better rates. Focus on:

i. Regular equipment checks

ii. Staff training

iii. Hazard reporting

iv. Updated safety policies

v. Fewer accidents mean fewer claims.

Common Mistakes Businesses Make

Many UK businesses unintentionally create serious insurance problems.

Assuming Public Liability Insurance Is Enough.

Public liability insurance protects against claims from customers or the public. It does NOT replace employers’ liability insurance.

You often need both. Forgetting Temporary Workers Count and Even temporary or seasonal staff may require coverage. This mistake commonly affects:

i. Restaurants

ii. Retail shops

iii. Event businesses

iv. Construction companies

Choosing the Cheapest Policy Only

Very cheap policies sometimes include:

i. Lower protection

ii. More exclusions

iii. Poor claims support

Cost matters, but coverage quality matters too.

How Claims Affect Future Insurance Costs

One serious claim can impact premiums for years. Insurers may view your business as:

i. Higher risk

ii. Poorly managed

iii. Unsafe for employees

After major claims, businesses often experience:

i. Higher renewal costs

ii. Reduced insurer options

iii. Larger excess requirements

Preventing claims is one of the best long-term cost-saving strategies.

Is Employers’ Liability Insurance Worth the Cost?

For most businesses, absolutely. Many business owners focus only on the yearly premium without considering the true financial risk of operating uninsured. A serious employee injury claim can involve legal costs. Some of the example under legal costs includes:

i. Compensation payouts

ii. Business interruption

iii.Reputation damage

iv. Regulatory investigations

Compared to these risks, even a £1,000 yearly premium becomes relatively small. Insurance is not just about legal compliance. It is about protecting the future of the business itself.

https://nittybrain.com

Final Thoughts on Employers’ Liability Insurance UK Cost.

The real cost of employers’ liability insurance in the UK depends on your business size, industry, payroll, and safety record. For low-risk businesses, coverage may cost less than many owners expect. For high-risk industries, premiums can be significant — but the cost of going uninsured can be catastrophic.

The most successful businesses treat employers’ liability insurance as a core protection strategy rather than just another expense.

A single workplace accident can happen in seconds. The financial consequences can last for years. If you employ staff in the UK, securing proper employers’ liability coverage is not simply a legal obligation — it is one of the smartest financial decisions a business owner can make.