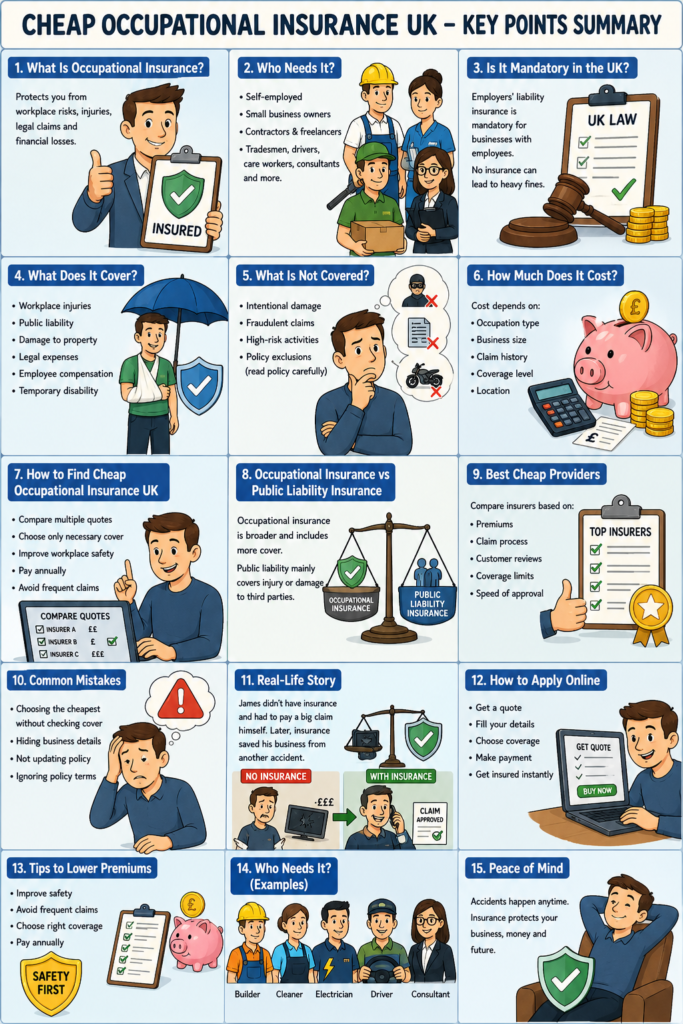

Cheap Occupational Insurance UK: How to Find Affordable Cover Without Sacrificing Protection

Finding Cheap Occupational Insurance UK policies can feel stressful, especially when you are trying to protect your business while keeping costs low.

Many workers, freelancers, and small business owners worry about paying high insurance premiums every month.

At the same time, nobody wants to face a legal claim or workplace accident without proper cover.

That is why choosing the right occupational insurance matters more than ever in the UK.

Whether you are a contractor, self-employed worker, tradesman, cleaner, consultant, or delivery driver, affordable insurance can protect your finances and your future.

This guide explains everything in simple English.

You will learn what occupational insurance is, who needs it, how much it costs, and how to find cheap occupational insurance quotes in the UK.

What Is Occupational Insurance?

Occupational insurance is a type of protection designed for workers and businesses.

It helps cover financial losses linked to workplace risks, accidents, injuries, or legal claims.

For example, imagine a self-employed electrician working in London.

While installing wires in a client’s house, an accidental fire damages part of the property.

Without insurance, the electrician may have to pay thousands of pounds from personal savings.

With occupational insurance, the insurer may help cover the costs.

This type of cover is especially useful for people whose jobs involve physical work, customer interaction, or professional advice.

Occupational insurance may include:

i. Employers’ liability insurance

ii. Public liability insurance

iii. Professional indemnity insurance

iv. Workplace injury cover

v. Legal expenses protection

Different occupations require different levels of protection. That is why comparing policies carefully is important.

Cheap Occupational Insurance UK for Self-Employed Workers

Self-employed workers often think insurance is too expensive. The truth is that many UK insurers now offer affordable policies for freelancers and sole traders. If you work independently, one legal claim could seriously damage your finances.

A freelance plumber, for example, may accidentally flood a customer’s kitchen during repairs. Even a small mistake could lead to compensation claims worth thousands of pounds.

Cheap occupational insurance helps reduce that risk.

Many self-employed workers choose basic policies first and upgrade later as their businesses grow.

This approach helps control costs while still providing protection.

Common professions that need cover include:

i. Builders

ii. Cleaners

iii. Electricians

iv. Carpenters

v. Delivery drivers

vi. Care workers

vii. Consultants

viii. Freelancers

Who Needs Occupational Insurance in the UK?

Many people assume only large companies need insurance. That is not true.

Even small businesses and independent workers can face expensive claims.

You may need occupational insurance if:

i. You work directly with customers

ii. You use tools or equipment

iii. You visit client properties

iv. You hire employees

v. You give professional advice

vi. You handle expensive goods

For example, a cleaner working in Manchester accidentally damages a client’s marble floor with the wrong chemical product. The client demands compensation.

Without insurance, the cleaner pays personally.

With cover, the insurer may handle the claim.

That is why occupational insurance provides peace of mind.

Is Occupational Insurance Mandatory in the UK?

Some types of insurance are legally required in the UK.

For example, employers’ liability insurance is mandatory for most businesses with employees.

If a company fails to carry proper cover, fines can become very expensive.

However, self-employed individuals without employees may not legally need it.

Still, many clients prefer hiring insured professionals.

Having insurance also makes your business appear more trustworthy and professional.

Imagine two contractors bidding for the same project. One has insurance and the other does not.

Most clients will choose the insured contractor because it reduces risk.

What Does Cheap Occupational Insurance UK Cover?

Different policies offer different protections.

However, most occupational insurance plans cover common workplace risks.

Typical coverage may include:

i. Workplace injury claims

ii. Public liability claims

iii. Damage to client property

iv. Legal expenses

v. Employee accidents

vi. Compensation claims

For instance, a delivery driver slips while carrying a customer’s parcel and damages expensive electronics.

The customer may demand repayment.

Insurance helps reduce the financial burden.

Some policies also include temporary disability protection.

This helps workers who cannot continue working after an accident.

How Much Does Occupational Insurance Cost in the UK?

The price depends on several factors. These include:

i. Occupation type

ii. Business size

iii. Number of employees

iv. Claim history

v. Coverage level

vi. Business location

Low-risk professions usually pay lower premiums.

High-risk industries like construction often pay more.

A freelance writer may pay very little each month.

A roofing contractor may pay significantly more due to higher workplace risks. Many small UK businesses find affordable policies starting from low monthly costs.

Comparing quotes is one of the best ways to save money.

How to Find Cheap Occupational Insurance UK

Finding affordable cover requires patience and smart comparison.

Here are some practical tips.

i. Compare Multiple Quotes

ii. Never buy the first policy you see. Different insurers offer different prices for similar coverage. Even saving a few pounds monthly can help long term.

iii. Choose Only Necessary Coverage

Some businesses pay for protection they do not actually need.

vi. Focus on risks directly related to your work.

Improve Workplace Safety

Businesses with safer work environments often receive lower premiums. For example, construction companies with strong safety records may qualify for discounts.

Pay Annually Instead of Monthly

Some insurers charge extra for monthly payment plans.

Annual payments may reduce overall costs.

Avoid Frequent Claim

Too many claims can increase future premiums. Small issues may sometimes be cheaper to resolve privately.

Best Cheap Occupational Insurance Providers In UK

Many insurers in the UK provide affordable occupational insurance.

The best provider depends on your profession and business size.

When comparing providers, consider:

i. Premium costs

ii. Claim process

iii. Customer reviews

iv. Coverage limits

v. Optional add-ons

vi. Speed of policy approval

Some online insurers now provide instant quotes within minutes. This makes it easier for busy professionals to get covered quickly.

Common Mistakes People Make When Buying Insurance

One major mistake is choosing the cheapest policy without checking coverage.

Cheap does not always mean good value. Another mistake is hiding business details to reduce premiums. This may lead to rejected claims later.

Some workers also fail to update policies when their business grows. For example, hiring employees without updating your insurance could create serious legal problems.

Always review your policy regularly.

Real-Life Story: Why Occupational Insurance Matters

James was a self-employed carpenter in Birmingham. He believed insurance was unnecessary because he had never faced legal problems before.

One day, while fitting shelves in a customer’s home, a heavy unit fell and damaged an expensive television.

The customer demanded compensation.

James had to pay from personal savings because he lacked insurance.

The situation affected his business finances for months. Later, he purchased occupational insurance.

A year afterward, another accident happened on a different project. This time, the insurer handled the costs.

James said the insurance saved his business from major financial stress.

Frequently Asked Questions

What is the cheapest occupational insurance in the UK?

The cheapest policies usually depend on your profession and risk level.

Low-risk jobs like consulting or freelance writing often cost less than construction or roofing work.

Comparing quotes from multiple insurers is the best way to find affordable coverage.

Can self-employed workers get occupational insurance?

Yes.

Many UK insurers offer occupational insurance specifically for freelancers, sole traders, and contractors. Even if you work alone, insurance can protect you from costly claims and accidents.

Is occupational insurance tax deductible in the UK?

In many cases, business insurance premiums may qualify as allowable business expenses.

This means businesses may reduce taxable profits by including insurance costs. It is always wise to speak with an accountant for accurate tax advice.

Does occupational insurance cover legal expenses?

Many policies include legal expense protection.

This may help pay solicitor fees, court costs, or compensation claims linked to workplace incidents.

Always check policy details carefully before buying.

How quickly can I get occupational insurance cover?

Some online insurers provide instant quotes and same-day coverage.

This is especially useful for contractors who need proof of insurance quickly before starting projects.

Is occupational insurance worth it for small businesses?

Absolutely.

Even small businesses face risks every day.

One accident or legal claim could create financial problems that take years to recover from.

Insurance provides financial protection and peace of mind.

Final Thoughts on Cheap Occupational Insurance UK

Finding reliable and affordable insurance does not have to be complicated. The key is understanding your risks and comparing policies carefully.

Cheap occupational insurance can protect your business, reputation, and finances when unexpected situations happen.

Whether you are self-employed, running a small business, or working as a contractor, having proper cover can make a huge difference.

A single accident may happen in seconds.

But the financial impact could last for years without insurance protection.