Employers’ Liability Insurance Certificate UK: Complete Guide for Businesses.

Running a business comes with many responsibilities. One important legal requirement is having an Employers’ Liability Insurance Certificate UK.

Many business owners ignore this document until they face inspections, penalties, or employee injury claims. That mistake can become very expensive.

If you employ staff in the UK, even part-time workers, you may legally need employers’ liability insurance.

The certificate proves your business has proper insurance cover for employee injuries or illnesses connected to work. For example, imagine a warehouse employee slips on a wet floor and breaks a leg.

Without the right insurance, the employer may personally face huge compensation costs.

This guide explains everything in simple English. You will learn the legal rules, costs, display requirements, common mistakes, and how to stay compliant.

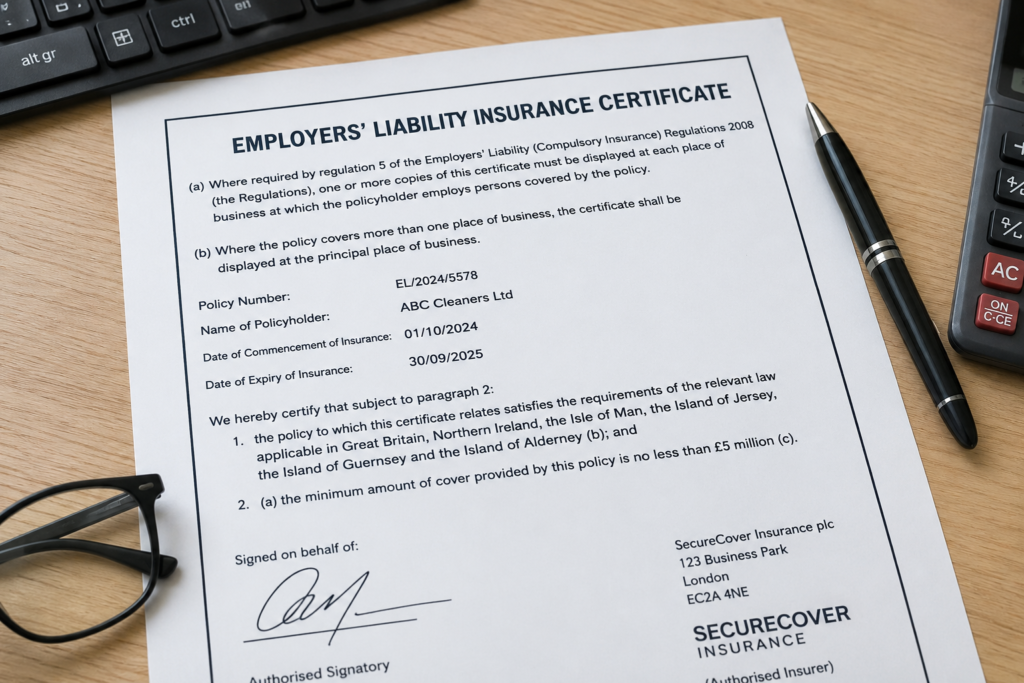

What Is an Employers’ Liability Insurance Certificate?

An employers’ liability insurance certificate is an official document from your insurer. It proves your business has employers’ liability insurance coverage.

The certificate usually contains:

i. Business name

ii. Insurance company details

iii. Policy number

iv. Coverage amount

v. Policy start and expiry dates.

In the UK, most employers must have at least £5 million of cover. Many insurers automatically provide digital certificates by email. Some also send printable PDF copies.

Think of the certificate like a driving licence for your business. It proves you are legally allowed to employ workers safely.

Employers’ Liability Insurance Certificate UK Requirements

The law behind this insurance is called the Employers’ Liability (Compulsory Insurance) Act 1969. Under UK law, employers must protect employees if they become injured or ill because of work activities. For example:

i. A construction worker falls from scaffolding

ii. A cleaner develops breathing problems from chemicals

iii. An office worker suffers injury from faulty equipment.

Without insurance, compensation claims could financially destroy a small business. This is why the government takes the law seriously.

If you fail to carry employers’ liability insurance, fines can reach £2,500 for every day you are uninsured.

Businesses can also face additional penalties for failing to display the certificate properly.

Who Needs Employers’ Liability Insurance in the UK?

Most UK businesses with employees need this insurance. This includes:

i. Small businesses

ii. Limited companies

iii. Shops

iv. Restaurants

v. Construction companies

vi. Cleaning businesses

vii. Care agencies

Viii. Hospitality businesses

ix. Even temporary workers and part-time staff may count as employees.

Many startup owners wrongly assume they do not need insurance because they only hired one person. That assumption can become a legal problem very quickly.

However, some businesses may be exempt. Examples include:

i. Family businesses with only close relatives employed

ii. Public organisations

iii. Some directors-only companies

Always confirm your status with a qualified insurance provider.

Employers’ Liability Insurance Certificate UK Display Rules

Many employers ask an important question. Where should the certificate be displayed?

The law requires employees to have reasonable access to the certificate. Years ago, businesses displayed paper copies on office notice boards.

Today, electronic copies are legally acceptable in many cases. For example:

i. Company intranet

ii. Shared staff portal

iii. Internal email systems

This is especially useful for remote workers and hybrid businesses. If an inspector requests proof of insurance, you should be able to provide it quickly. Failing to display the certificate properly can lead to fines.

A smart business owner keeps both digital and printed copies available.

Can Employers Liability Certificate Be Displayed Electronically?

Yes.

UK law allows electronic display of employers’ liability certificates. This became increasingly important after remote work became common.

Employees must still have easy access to the document. For example, if your workers cannot access the company portal from home, you may not fully meet compliance requirements. Good practice includes:

i. Sending employees a direct PDF copy

ii. Keeping certificates in shared HR folders

iii. Providing mobile-friendly access

Electronic storage also makes record keeping easier. Some companies keep old certificates for decades because past employees may later make injury claims.

Employers Liability vs Public Liability Insurance

Many people confuse these two insurance types. But they protect against different risks.

Employers’ Liability Insurance

This protects employees. Example: A worker injures their back while lifting heavy equipment.

Public Liability Insurance

This protects against claims from the public. Example: A customer slips on a wet supermarket floor.

Many UK businesses need both types of cover. For example, a café may need:

a. Employers’ liability insurance for staff

b. Public liability insurance for customers

Having one policy does not automatically replace the other.

Employers Liability Insurance Cost UK

The cost depends on several factors. These include:

i. Number of employees

ii. Business type

iii. Industry risk level

iv. Claims history

V. Annual payroll

Low-risk office businesses may pay much less than construction firms. For example:

Small office company: lower premium, roofing contractor. higher premium Insurance companies calculate risk carefully.

Businesses with strong workplace safety systems often receive better pricing. Comparing multiple insurance quotes can save money.

How to Get an Employers’ Liability Insurance Certificate UK

The process is usually simple.

Step 1: Gather Business Information

You may need employee numbers, payroll estimates, business activities, claims history to gather business information.

Step 2: Compare Insurance Providers

Look for good customer support, fast certificate delivery, clear policy wording. This are the quality ways to get an insurance provider.

Step 3: Purchase the Policy

After payment, the insurer issues your certificate. Many companies now provide instant downloadable PDFs.

Step 4: Display the Certificate

Ensure employees can easily access it. That must be after getting the certificate.

Real-Life Example

A small electrical company in Manchester hired two temporary workers during a busy season. The owner assumed temporary staff did not count as employees.

During a routine inspection, authorities requested proof of employers’ liability insurance. The business had none. The owner later received heavy fines and rushed to purchase emergency cover. The situation became stressful and expensive.

A simple insurance policy could have prevented the entire problem.

Common Mistakes Businesses Make

Assuming One Employee Does Not Matter. Even one employee may trigger legal requirements. Forgetting to Renew Policies, expired insurance can still lead to penalties.

Ignoring Remote Workers. Remote staff still need access to the certificate.

Misunderstanding Exemptions. Many businesses wrongly assume they qualify for exemptions.

Keeping Poor Records. Missing documents create problems during inspections and claims.

Employers Liability Insurance for Small Business UK

Small businesses are often most vulnerable to legal claims. One serious workplace injury could create huge financial pressure. For example, a small bakery employee burns their hand using faulty equipment. Medical costs and compensation claims can become expensive quickly.

Employers’ liability insurance helps protect small business owners from these risks. It also builds trust with employees. Workers feel safer knowing the business takes protection seriously.

What Happens If You Don’t Have Employers Liability Insurance?

The consequences can be severe. Possible penalties include:

i. Daily fines

ii. Legal investigations

iii. Compensation claims

iv. Business reputation damage

In serious situations, a single employee injury claim may bankrupt a business. Insurance acts as financial protection during unexpected situations. That is why compliance matters so much.

Frequently Asked Questions

Is employers liability insurance compulsory in the UK?

Yes.

Most businesses with employees legally need employers’ liability insurance under UK law. Failure to comply can result in significant daily fines.

Can I show my employers liability certificate online?

Yes.

Electronic display is legally accepted if employees can access the certificate easily. Many companies now use staff portals or shared internal systems.

Do sole traders need employers liability insurance?

Usually not if they work alone.

However, once a sole trader hires staff, legal requirements may apply. Always confirm with an insurance professional.

How long should old employers liability certificates be kept?

Many experts recommend keeping old certificates permanently. Some employee illnesses or injury claims may appear years later. Old records can help protect businesses during disputes.

What is the minimum employers liability insurance cover in the UK?

The legal minimum is usually £5 million.

However, many insurers automatically provide £10 million cover.

Does employers liability insurance cover temporary workers?

Yes in many situations.

Temporary staff, casual workers, and part-time employees may still count as employees under the law.

What happens if an employee gets injured at work?

The employee may file a compensation claim. Employers’ liability insurance helps cover legal costs and compensation payments. Without insurance, the employer may personally face those financial losses.

Final Thoughts

Understanding the Employers’ Liability Insurance Certificate UK requirements is extremely important for every employer. Many businesses only realize its importance after facing penalties or claims.

A simple insurance policy can protect your company, employees, finances, and reputation. Staying compliant is not just about following the law.

It also shows responsibility and professionalism. Whether you run a small startup or a growing company, having the right insurance cover gives peace of mind for the future.