Windstorm exclusion buyback option

NittyBrain Insurance Desk

The Windstorm Exclusion Buyback Option: How Coastal Homeowners Are Quietly Buying Back the Coverage Insurers Tried to Take Away

One line in your policy can leave your roof, your siding, and your savings completely unprotected the next time the wind picks up. Here’s the option most agents never mention — and exactly how homeowners and Travelers policyholders can get it back.

Fast answer: A windstorm exclusion buyback option is an endorsement or standalone policy that lets a homeowner reinstate wind and hail coverage that was removed from their policy, or reduce the separate wind deductible that applies to hurricane and tropical storm claims. If your homeowners or Travelers policy carries a wind exclusion, this is the mechanism that puts your roof back under real protection. Check your windstorm buyback eligibility with Travelers →

Somewhere between the fine print and the renewal notice, thousands of homeowners in coastal states find out the hard way: their policy has a wind exclusion. Not a higher deductible. Not a sub-limit. A flat exclusion — meaning if a named storm tears the shingles off your roof, your insurer owes you nothing for that damage. It happens quietly, usually after an insurer pulls back from a hurricane-exposed ZIP code, and most homeowners don’t notice until they’re standing in a driveway full of debris reading a denial letter.

The good news is that a wind exclusion is not always permanent. In most cases, it can be bought back — either by adding a windstorm exclusion buyback endorsement to your existing homeowners policy, or by layering a standalone wind buyback policy on top of it. This guide breaks down exactly how the windstorm exclusion buyback option works, what it costs, how it differs from a simple deductible buydown, and how homeowners and Travelers policyholders specifically can put it in place before the next storm season — not after.

What a Windstorm Exclusion Actually Means for Your Policy

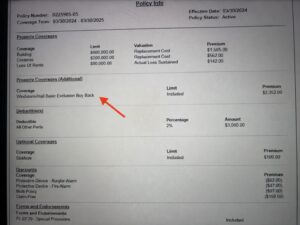

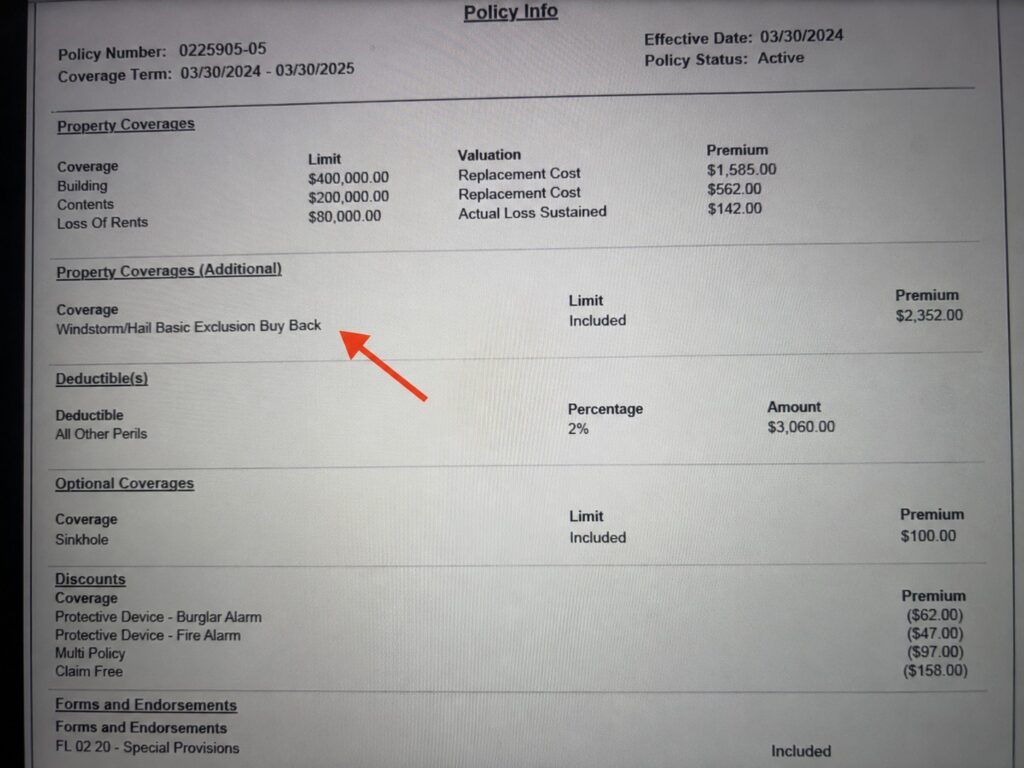

Most standard homeowners policies, including Travelers’ HO-3 form, list windstorm and hail as a named peril — meaning wind damage to your dwelling, siding, and roof is covered by default. But in coastal and catastrophe-prone counties, some carriers strip wind out entirely and replace it with an exclusion clause, or they attach a separate, much higher percentage-based deductible that only kicks in for named storms.

Both situations create the same problem: a gap between what you assume you’re covered for and what your insurer will actually pay after a windstorm. A windstorm exclusion buyback option exists specifically to close that gap, whether the goal is restoring full wind coverage or shrinking the dollar amount you’d owe out of pocket before coverage begins.

Two Different Products Hide Under the Same Name

This is where most articles on this topic get sloppy — and where homeowners end up buying the wrong thing. “Buyback” gets used for two related but distinct products:

| Type | What It Does | Best For |

|---|---|---|

| Windstorm exclusion buyback (coverage buyback) | Reinstates wind/hail as a covered peril on a policy that currently excludes it entirely. | Homes with a full wind exclusion, often in Gulf Coast and Atlantic coastal zones. |

| Wind deductible buyback (buydown) | Lowers a high percentage-based hurricane/wind deductible (often 1%–5% of dwelling value) to a flat, manageable dollar amount. | Homes that already have wind coverage but face a steep named-storm deductible. |

If your declarations page says wind and hail are excluded, you need the first product. If wind is covered but your named-storm deductible is 2%–5% of your dwelling limit — which on a $400,000 home is $8,000–$20,000 due before your insurer pays a cent — you need the second. Many coastal homeowners eventually need both.

Why Homeowners Insurers — Including Travelers — Started Excluding Wind in the First Place

Wind and hail losses have outpaced almost every other homeowners claim category over the past decade. As reconstruction costs climbed and storm frequency increased along the Gulf and Atlantic coasts, carriers responded the way any risk-bearing business does: they narrowed what they’d absorb without a separate premium. That’s shown up as higher named-storm deductibles industry-wide, and in the highest-risk tiers, outright wind exclusions paired with an optional buyback.

Travelers homeowners policies are built around named perils for personal property and open-peril dwelling coverage, with windstorm and hail explicitly listed among the covered causes of loss on a standard HO-3. Where state regulators or reinsurance treaties require it in the highest-risk counties, that coverage can be modified through endorsement — which is exactly where a windstorm exclusion buyback option becomes relevant to a Travelers policyholder specifically. If you’re unsure whether your policy carries a wind exclusion or an elevated named-storm deductible, your declarations page and the “Exclusions” section of your policy booklet will spell it out in a few short lines.

What Determines the Price of Your Buyback

There’s no flat-rate answer here, but the variables that move the price are consistent across every carrier and every state:

- Distance from the coastline. Properties within a mile or two of open water carry the steepest buyback premiums.

- Roof age and construction. Newer roofs rated for high wind speeds, hip roofs, and impact-resistant shingles can meaningfully lower the cost.

- Wind mitigation features. Hurricane straps, storm shutters, reinforced garage doors, and impact windows are the fastest way to shrink your premium.

- The size of the buydown. Buying a 5% deductible down to 1% costs more than buying it down to 3%. You’re purchasing dollars of protection, not a flat product.

- Your home’s total insured value. Since wind deductibles are typically percentage-based, the buyback premium scales with your dwelling coverage limit.

As a rough industry benchmark, minimum premiums for standalone wind or deductible buyback coverage tend to start in the low hundreds of dollars and climb from there depending on coastal exposure and the size of the buydown — which is a small fraction of the tens of thousands of dollars a high wind deductible could otherwise leave you owing after a single storm.

How to Get a Windstorm Exclusion Buyback in Place — Step by Step

- Pull your current declarations page and check the “Perils Insured Against” and “Exclusions” sections for wind or hail language.

- Identify which product you need using the table above — full reinstatement of wind coverage, or a deductible buydown.

- Ask your carrier directly whether a windstorm exclusion buyback endorsement is available in your state and county. Travelers policyholders can confirm eligibility and request a quote through their agent or online. Get a Travelers homeowners quote here →

- If your primary carrier can’t offer it, ask about a standalone wind policy that layers on top of your existing homeowners coverage — this is common in the highest-risk coastal tiers.

- Time it before hurricane season. Most carriers won’t bind new wind coverage once a named storm is already forming in the Atlantic or Gulf, so the window to buy back your protection closes fast every year.

Homeowners vs. Travelers Buyers: What Actually Changes

The mechanics of a windstorm exclusion buyback option are the same everywhere, but the paperwork differs by carrier. Homeowners with policies outside Travelers may need to shop a surplus-lines or specialty market to find buyback capacity, since not every standard carrier writes it directly. Travelers policyholders have an advantage here: windstorm and hail are already named perils on the standard HO-3 form, so in most non-excluded territories you’re simply adjusting a deductible rather than fighting to reinstate a peril from scratch — which typically makes the buyback conversation faster and the underwriting less invasive.

Don’t wait for the next named storm to find out what your policy excludes.

Get a windstorm exclusion buyback quote and see exactly what it would take to close your coverage gap.

Frequently Asked Questions

Is a windstorm exclusion buyback the same as flood insurance?

No. Wind and flood are separate perils in virtually every policy. A windstorm buyback restores or improves wind and hail protection only. Storm surge and rising water require a separate flood insurance policy, typically through the NFIP or a private flood carrier.

Can I add a windstorm exclusion buyback mid-policy, or only at renewal?

Many carriers allow it to be added mid-term, but availability narrows sharply once a storm is already being tracked toward your region. The safest window is well before hurricane season begins.

Does a mortgage lender ever require a windstorm buyback?

Yes. In high-risk coastal counties, lenders sometimes require a deductible below a certain threshold as a condition of the loan or a refinance. A buyback is frequently the fastest way to meet that requirement without switching carriers.

Will wind mitigation upgrades lower my buyback premium?

Generally, yes. Impact-rated roofing, hurricane straps, storm shutters, and reinforced garage doors are the upgrades carriers most consistently reward with lower buyback and buydown premiums.

About this research: This guide was researched and written by the NittyBrain insurance desk, drawing on current carrier policy documentation, state insurance department filings, and industry deductible-buyback data. NittyBrain covers insurance and personal finance topics to help homeowners make informed, unbiased coverage decisions. This article is for general informational purposes and is not a substitute for reviewing your own policy documents or speaking with a licensed insurance professional.